GST Refund on Inverted ITC: Real Case Study of a Kids’ Tricycle Manufacturer (5% Output vs 18% Inputs)

GST refunds under the Inverted Duty Structure are among the most common refund claims filed by manufacturers in India. Such situations arise when the GST rate on inputs is higher than the GST rate applicable on the final product, resulting in accumulation of Input Tax Credit (ITC) that cannot be fully utilized against output tax liability.

Although the GST law permits refund of such unutilized ITC, the practical process of obtaining the refund often requires detailed clarification and documentation. In many cases, the GST department seeks technical explanations to verify whether the refund claim genuinely arises due to the inverted duty structure.

At Our Financial Advisor, drawing from our experience in handling GST refund matters, we are sharing insights from a recently handled case involving a manufacturer of kids’ tricycles, where the refund arose due to the inverted tax structure between inputs taxed at 18% and output supplies taxed at 5%.

This case highlights how proper documentation, technical explanation, and a structured response to departmental queries can significantly improve the chances of successful GST refund processing.

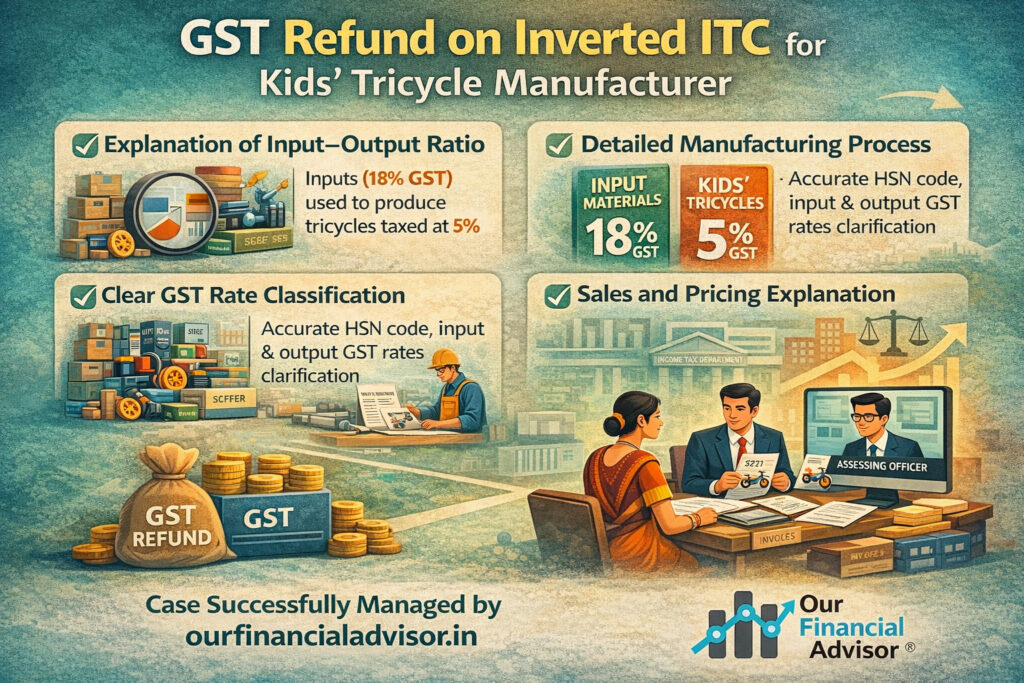

Understanding the Inverted Duty Structure in This Case

Our client was engaged in the manufacturing and sale of kids’ tricycles.

Under GST, kids’ tricycles are taxed at 5%, whereas many of the raw materials used in manufacturing attract 18% GST. Because of this difference in tax rates, the client regularly accumulated excess Input Tax Credit.

The major inputs used in manufacturing included:

Plastic molded components

Steel pipes and metal frames

Rubber wheels and fittings

Nuts, bolts, and mechanical parts

Packaging materials and paints

Since the GST paid on purchases was significantly higher than the GST payable on sales, the business accumulated ITC over time, making it eligible to claim a refund under the inverted duty structure provisions of GST law.

Legal Framework Governing Inverted ITC Refund

The refund application was filed in accordance with the GST provisions and procedural guidelines issued by the government, particularly:

Circular No. 125/44/2019 – GST (Procedure for GST refunds)

Circular No. 135/05/2020 – GST (Clarification on refund restrictions)

The refund mechanism itself is governed under Rule 89(5) of the CGST Rules, which prescribes the formula for calculating refund of unutilized ITC in case of inverted duty structure.

Despite filing the refund claim in accordance with these provisions, the GST department sought additional clarification regarding the business operations and ITC accumulation.

Department Queries During Refund Processing

During the verification of the refund application, the department raised certain queries to understand the genuineness of the inverted tax structure.

The officer requested detailed clarification on the following aspects:

Input–Output Ratio of raw materials and finished goods

Manufacturing process of kids’ tricycles

GST rate classification of inputs and finished goods

Sales structure and pricing mechanism

Such queries are common in refund cases because the department needs to ensure that ITC accumulation is genuine and arises due to tax rate differences rather than incorrect classification or reporting.

Our Strategic Approach to Address Department Queries

Instead of providing generic responses, we prepared a comprehensive technical explanation supported by proper documentation and reconciliations.

1. Input–Output Ratio Analysis

A detailed working was prepared showing:

Quantity of raw materials used

Production output of finished tricycles

Consumption pattern of components

This clearly demonstrated that the ITC accumulation was directly linked to the actual production process.

2. Detailed Manufacturing Process Explanation

We provided a step-by-step explanation of the manufacturing process of kids’ tricycles, including:

Procurement of steel pipes and plastic components

Frame fabrication and welding

Installation of wheels, pedals, and steering components

Painting and finishing process

Final assembly and packaging

This helped the department understand how inputs taxed at 18% are used to manufacture finished goods taxed at 5%.

3. GST Rate Classification Clarification

We also submitted detailed clarification regarding:

HSN classification of raw materials

HSN classification of finished goods

Applicable GST rates on both inputs and outputs

This ensured that the department had complete clarity regarding tax rate differences causing the inverted structure.

4. Explanation of Sales Structure

To provide a complete understanding, we also explained:

GST charged on the sale of tricycles

Pricing structure of finished products

Reason for continuous accumulation of ITC

This demonstrated that the refund claim arose purely due to the inverted tax structure and not due to any reporting error.

Successful Outcome of the GST Refund Case

After reviewing our detailed explanations and supporting documents, the GST department was satisfied that:

The inverted duty structure was genuine

ITC accumulation was legitimate

GST classifications were correctly applied

As a result, the refund claim was successfully processed and approved, resulting in a favourable outcome for the client.

Key Takeaway for Businesses Claiming GST Refund

This case highlights an important practical lesson for businesses:

GST refund claims require more than just filing an application on the GST portal.

To ensure successful processing, businesses often need to demonstrate:

Proper manufacturing process explanation

Logical input–output relationship

Correct GST rate classification

Clear justification for ITC accumulation

A well-structured and technically sound response can significantly reduce delays and objections during the refund verification process.

Our Expertise in GST Refund Advisory

At Our Financial Advisor, we assist businesses across industries in handling complex GST matters, including:

GST Refund under Inverted Duty Structure

GST Refund Documentation and Filing

Handling GST Department Queries

GST Notices and Litigation Support

GST Compliance and Advisory Services

Our objective is to help businesses secure legitimate GST refunds while ensuring full compliance with tax laws.